BOURBON Investor Presentation May 2014 BUILDING TOGETHER A SEA OF TRUST

|

|

|

- Erik Willis

- 5 years ago

- Views:

Transcription

1 BOURBON Investor Presentation BUILDING TOGETHER A SEA OF TRUST

2 DISCLAIMER This document may contain information other than historical information, which constitutes estimated, provisional data concerning the financial position, results and strategy of BOURBON. These projections are based on assumptions that may prove to be incorrect and depend on risk factors including, but not limited to: foreign exchange fluctuations, fluctuations in oil and natural gas prices, changes in oil companies investment policies in the exploration and production sector, the growth in competing fleets, which saturates the market, the impossibility of predicting specific client demands, political instability in certain activity zones, ecological considerations and general economic conditions. BOURBON assumes no liability for updating the provisional information based on new information in light of future events or any other reason. 2

3 SUMMARY Introduction to BOURBON 4 13 Strengthening our position further Outlook Appendices

4 Introduction to BOURBON 4

5 Servicing offshore oil & gas industry MARINE SERVICES Terminal tugs dedicated to assistance and operations on offshore oil and gas terminals MARINE SERVICES Assistance and salvage tugs dedicated to preventing wrecks, assisting and salvaging vessels in distress, and fighting pollution risks. MARINE SERVICES AHTS (Anchor Handling Tug Supply vessels) ensure the implementation and maintenance of oil and gas platforms. SUBSEA SERVICES IMR Vessels support for subsea operations and surface interventions, and Inspection, Maintenance and Repair operations in ultra deepwater oil fields. MARINE SERVICES Crewboats FSVIV (Fast Support and Intervention Vessels) for emergency supplies and the transport of emergency service teams, and surfers for the transport of staff to oil & gas platforms. MARINE SERVICES PSV (platform supply vessels) supply equipment and special products to offshore platforms. SUBSEA SERVICES ROV (undersea robots) conduct a broad range of Inspection, Maintenance and Repair operations on Subsea structures. 5 5

484 offshore vessels* (end 2013) > 11 100 employees (end")

6 A unique investment strategy BOURBON offshore vessels (end 2002) employees (end 2002) 484 offshore vessels* (end 2013) > employees (end 2013) 3 customers = 76% 2002 revenues 5 customers = 49 % 2013 revenues Afrique revenues breakdown 85% in 2002 Afrique revenues breakdown 57% in 2013 Revenues (in m) Number of vessels Σ offshore capex: 4.8 bln Number deliveries Total Crew + FSIV Total Supply TOTAL FLEET * Vessels operated by BOURBON (including vessels owned or on bareboat charter)

7 A modern and standardized fleet in line with market needs, Modern fleet 484 vessels in operation 6.2 years average age 52 vessels on order Investment strategy: Standardization High manoeuvrability: DP2 Energy savings: Diesel Electric Construction in series BE 502 on sea trials 81% of the fleet* fully aligned with the BOURBON investment strategy * Figures as at 12/31/2013, excluding Crewboats 7

8 Benefits of standardization SUBSEA DEEPWATER SHALLOW WATER CREWBOATS FLEET 10 BE GPA B Explorer B Liberty PSV 74 B Liberty AHTS 40 Surfer Surfer 1800 COMMON EQUIPMENT KW1235 KW1825 KW2000 KW662 TRAINING 2 offshore simulators 8 Surfer simulators REPAIR & MAINTENANCE B. Black Sea B. Docking B. Sourcing & Trading 6 Repair Centers 15 Shipmanagers SPARE PARTS PLUG & PLAY / SHOW STOPPERS 8

9 BOURBON: key drivers to master growth Innovation Determination Implementation

in Asia")

10 A list of demanding customers throughout the world Mediterranean/ Middle East 25 Mexico/ Brazil 14 Number of vessels Dec 2013 Asia 25 West Africa 36 A global presence Bourbon Liberty Series Major 37% Contractors Others 7% 8% National Oil 28% Independents 19% Dec 2013 A performance recognized by customers 10 Bourbon Kaimook (BL 301) in Asia Bourbon Liberty 203 in the UAE

11 OSV Market bifurcates at fast pace OSV global utilisation by build age compared to Bourbon fleet Utilisation % Built in 1991 and earlier Built in 2005 and later BOURBON 0 11 Source : IHS Petrodata August

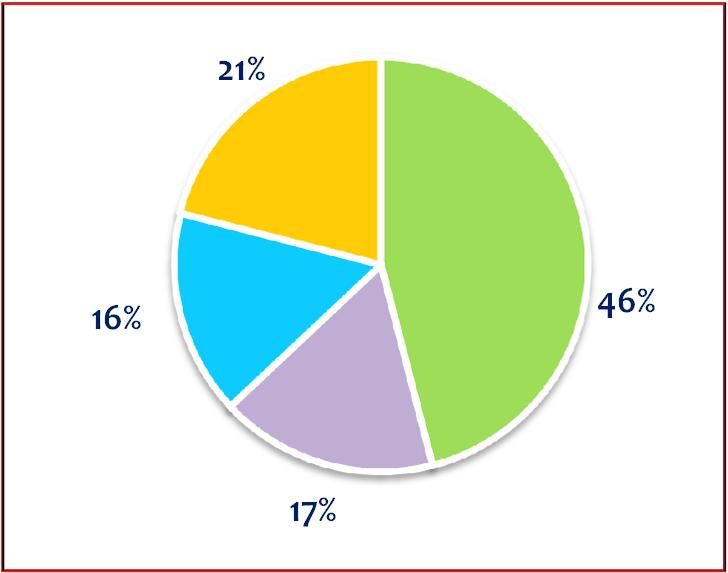

12 A diversified list of demanding customers NOCs SUPER MAJORS 21% 16% 46% 17% Other International Oil Cos, Independents Contractors 12 12

13 Safety results among the best in the industry 45.3 million hours worked in TRIR target by year TRIR: total recorded incidents rate per million hours worked on a 24/7 basis LTIR: lost time incidents rate per million hours worked on a 24/7 basis 13 13

14 Strengthening our position further 14

15 A leader in offshore maritime services: a global presence North Sea: 7 Supply vessels France: 8 Supply vessels and tugs 15 Changes vs 12/31/2012 (in number of vessels) Americas 31 Supply & Subsea vessels 23 Crewboats +1 West Africa 95 Supply & Subsea vessels 225 Crewboats +9 TOTAL 212 Supply & Subsea vessels 272 Crewboats Mediterranean Middle East India 39 Supply & Subsea vessels 4 Crewboats +9 South East Asia 32 Supply & Subsea vessels 20 Crewboats +10

16 Committed teams with strong local ties in Latin America, Africa and Asia Local content* reached 70% in ,000 hours of professional training delivered in 2013 BOURBON Europe Mediterranean Middle East Asia & Pacific 21% Europe 35% 24% 76% Africa 31% America 13% 11,149 people Americas 12% 88% 1,538 2,257 Africa 42% 58% Asia 17% 5,862 83% 1,492 * Proportion of employees working in their region of origin Employees 16

17 94.5% fleet technical availability rate Operational downtime Statutory maintenance In % Nr. of days / DD Average for the BOURBON fleet, excluding Crewboats An ever more reliable fleet, in line with our objectives to reach 95% technical availability in

18 Solid indicators in a growing market In % 100 Stable utilization rates and rising prices In US $ % $20,000 92% 90 87% $19,000 $18,000 $17,000 $16,000 $15, $14,000 $13, H H H H H H Average daily rate in US $ Utilization rate in % $12, Data for the Deepwater offshore and Shallow water offshore segments and for the Subsea business

19 Discipline in managing costs Operating costs Investment costs Crew Maintenance Dockings Others Total fleet Operating cost index Construction in series Standardization of equipment Optimization of order timing Reduce our costs to reduce our customers' costs 19

20 Key factors Fleet as of December 31, 2013 Operating vessels Average age Vessels on order TOTAL whollyowned on bareboat charter TOTAL Total Marine Services Deepwater offshore vessels Shallow water offshore vessels Crewboats Total Subsea Services Fleet TOTAL ROV

21 Expected deliveries Number of vessels (including vessels under construction as part of the agreement signed with ICBCL) Deliveries H Deliveries H Deliveries H Deliveries H TOTAL Valeur in m (excluding financial costs) Deepwater offshore vessels Shallow water offshore vessels Crewboats IMR vessels m 123m 127m 85m 396m m 46m 192m m 17m 40m m 90m 90 M 315m m 276m 217m 85m 943m 21

22 Active fleet management: Transforming for beyond Fleet concerned: recent supply vessels, with a well established standard Double operation Sale of vessels at market price of US$2.5 billion Bareboat chartering of the same vessels for 10 years For these customers, fleet availability ensured and operating standards maintained for 10 years Sales made gradually, at the rate of delivery from the shipyard 22

23 «Transforming for beyond» : Target US$2.5 billion US$1,650 million already signed as at March 5, 2014 With the Chinese company ICBC Leasing: 51 vessels for an amount of US$1.5 billion With Standard Chartered Bank: 6 vessels for an amount of US$150 million Target set Signed with ICBCL Signed with SCB Agreements to be concluded 23

24 Transforming for beyond: US$1,051 million already received to date** Target: sale of 30% of the supply vessel fleet by 2015 Vessel disposals and bareboat chartering (10 years) With ICBCL 36 vessels already sold US$986 million received With SCB 3 vessels already sold US$65 million received 24 Compliant vessels Partly compliant vessels Non compliant vessels *Conformity to standards of BOURBON: Diesel Electric propulsion, Dynamic Positioning class 2 ** as of April 30, 2014

With Pareto 2 vessels US$130 million received Compliant vessels Partly compliant vessels Non compliant")

25 Simultaneously, sale of vessels only partly compliant with the BOURBON technical standards Vessel disposals and bareboat chartering (5 years) With Pareto 2 vessels US$130 million received Compliant vessels Partly compliant vessels Non compliant vessels 25

26 and sales of old vessels Sales to other shipowners 5 vessels US$53 million received Sale of vessels Compliant vessels Partly compliant vessels Non compliant vessels 26

27 BOURBON fleet: average age 6.2 years Age profile by operating segment* Vessel count: Deepwater offshore 72 Shallow water offshore 122 Subsea Deep Shallow Subsea 27 * Excludes crewboats * Data as of December 31, 2013

28 Strong positive free cash flow* at 450m In millions * Free cash flow: Cash flows linked to operating activities outflows linked to purchases of property, plant and equipment and intangible assets + inflows linked to disposals of property, plant and equipment and intangible assets 28

")

29 449 million reduction in debt since June 30, 2013 ( millions) ,750 1,765 1,955 2,061 Net debt June 30, ,190 1, Dette nette Dette Nette/EBITDA 29

30 Outlook 30

on mid and deepwater offshore of 10% per annum over 2013 2018 period Average growth in expenditurse")

31 Outlook for Oil & Gas offshore market Demand for oil and gas is expected to grow 1.4% per annum over the period Average growth in expenditures (investment & operation) on mid and deepwater offshore of 10% per annum over period Average growth in expenditurse (investment and operation) on shallow water offshore of 7% over period Mid & deepwater E&P expenditure USD billion nominal + 10% per annum Shallow water E&P expenditure USD billion nominal + 7% per annum 31 Source: Rystad Favorable to demand for offshore vessels

32 Supply of shallow water offshore vessels AHTS (4,000 9,999 BHP) PSV (1,000 1,999 DWT) Number of vessels Future deliveries Current fleet Future deliveries Current fleet 97 on order Current fleet 1,372 Of which 388 > 25 years old Number of vessels on order Current fleet 316 Of which 141 > 25 years old 0 H H H H H H H H H H Competition BOURBON Competition BOURBON 97 vessels on order, i.e. 7% of the fleet in service 28% of the current fleet is over 25 years old and can no longer compete with modern vessels 36 vessels on order, i.e. 11% of the fleet in service 45% of the current fleet is over 25 years old and can no longer compete with modern vessels Growth in the supply of shallow water offshore vessels is low due to the effect of the replacement of old vessels 32 Source: IHS Petrodata January 2014

33 Supply of deepwater offshore vessels AHTS (> 10,000 BHP) PSV (> 2,000 DWT) Future deliveries Current fleet Future deliveries Current fleet Number of vessels H H H H H Competition 59 on order Current fleet 546 Of which 76 > 25 years old Number of vessels H H H H H H Competition > 4kDWT PSV Competition 2 3,9kDWT PSV BOURBON 2 3,9kDWT PSV Of which 37 > 25 years old 337 on order Current fleet vessels on order, i.e. 11% of the fleet in service 14% of the current fleet is over 25 years old and can no longer compete with modern vessels 337 vessels on order, i.e. 37% of the fleet in service 4% of the current fleet is over 25 years old and can no longer compete with modern vessels A growing supply of deepwater offshore vessels characterized by a large number of PSV vessels under construction, potentially affecting prices in this segment in Source: IHS Petrodata January 2014

; the first 6")

34 Outlook for AHTS and PSV vessels for the BOURBON fleet AHTS PSV Shallow water Offshore 87 vessels with a 73% contractualization rate 5 Bourbon Liberty under construction; the supply/demand balance and success of the series of 74 Bourbon Liberty will help to improve performance 34 vessels with an 85% contractualization rate 7 Bourbon Liberty under construction; a small market in terms of size (316 vessels) in which BOURBON is aiming on long term contractualization of its fleet AHTS PSV Deepwater offshore 13 vessels with a 68% contractualization rate BOURBON will not receive any new units in 2014 and 2015; the goal is to improve utilization rates through a higher long term contractualization of the fleet 31 vessels with a 79% contractualization rate The 19 Bourbon Explorer 500 under construction are suitable for high growth tropical offshore markets (Asia, India, Africa and South America); the first 6 vessels are contractualized 34

Sale of the Blue Angel")

35 Increasing Subsea activity in a growing market Market 10.3% growth in well head installations over the period Ageing of subsea equipment implies an increase in demand for IMR vessels. On average, the 5,000 well heads installed are now more than ten years old BOURBON Delivery of the BE 803 in the first half contractualized in Asia (Malaysia / New Caledonia) Sale of the Blue Angel in the 3 rd quarter Number of vessels in operation 18 vessels Contractualization rate 66.7% at December 31,

36 Conclusion Demand for offshore vessels sustained by high level of costs in the offshore Oil & Gas sector From now on, new orders for vessels will be executed as opportunities arise and will not impact revenues before 2016 Outlook for 2014: Revenue growth of 8% to 10% slight improvement in operating margin (EBIDTAR/revenues)* BOURBON is committed to reduce its debt and improve its profitability and shareholder return 449 million reduction in net debt in the 2 nd half 2013 Operating margin increased 2.1 pts in 2013 vs Proposed dividend of 1/share, +34% vs *EBITDAR = EBITDA excluding bareboat charter costs

37 APPENDICES 37

38 Growth and improvement of profitability Revenues Subsea 17% Others Deepwater offshore +10.5% Crewboats 22% 1,312 million 29% 30% 1,187 1,312 EBITDAR (excl. capital gains)/revenues Shallow water offshore 2012 In millions pts Subsea Crewboats 19% 21% EBITDAR (excl. capital gains) Others 450 million 26% 33% Deepwater offshore +17.6% % 34.3% Shallow 29% water offshore 2012 In millions

39 53 million in exchange losses in 2013, 65% of which unrealized In millions of euros Σ realized = ( 0.4 million) Realized Unrealized 60 H H H H H H

: test under way with three of")

40 "Transforming for beyond" : a unique and personalized customer relationship Real time tracking of vessel operational performance indicators available to our client (Web Platform): test under way with three of our customers : means dedicated to the success of our teams Launch of the second "Safety Takes me home" campaign Our team commitment rate rose by 8% between 2010 and 2013 : towards operational efficiency at controlled costs Centralization of group purchasing Standardization of the vessels' operation and reporting system 40

41 BOURBON Contractualization as of December 31, 2013 Contractualization rate Average residual term of firm contracts Average residual term including options Deepwater offshore vessels 77.8 % 11.8 months 22.3 months Shallow water offshore vessels 77.1% 12.3 months 18.4 months Crewboats 71.6 % na na IMR Fleet 66.7 % 13.9 months 21.5 months 41

42 Activity Key data 2013 Marine Services Subsea Services Deepwater offshore Shallow water offshore By Half Year Crewboats By Half Year H H H H H H H H Number of vessels Average utilization rate 88.4% 89.4% 89.4% 90.2% 79.3% 78% 89.2% 91.3% Average daily rate 21,789 $ 22,482 $ 14,078 $ 13,877 $ 5,083 $ 5,270 $ 40,262 $ 42,226 $ Availability rate 94.5% 95.9% 96.1% 96.1% 92.2% 95.29% 92.8% 94.1% 42

43 BOURBON shareholder structure Shareholder structure * Geographic breakdown 26% 3% 2% 2% 1% 1% 51% 8% 39% 52% 1% 4% 5% 5% Jaccar Holdings Monnoyeur SAS Treasury stock Public Mach Invest International Financière de l'échiquier Employees France Benelux Norway USA Europe Others UK Others * As of December 31,2013 source : Euroclear. CAIES. regulatory filings 43

B O U R B O N - R o a d s h o w A p r i l

BOURBON - Roadshow A p r i l 2 0 1 4 BUILDING TOGETHER A SEA OF TRUST DISCLAIMER This document may contain information other than historical information, which constitutes estimated, provisional data concerning

BOURBON - Roadshow A p r i l 2 0 1 4 BUILDING TOGETHER A SEA OF TRUST DISCLAIMER This document may contain information other than historical information, which constitutes estimated, provisional data concerning

Q Q Q Q Q % % 46.8% 61.0% 35.6% 57.5% 52.1% 60.5% 44.6% 63.3% 15,267 15,081 15,260 15,265 16,299

Press release Paris, May 4, 2017 BOURBON 1 st quarter 2017 financial information Adjusted revenues amounted to 225.5 million ( 204.9 million in consolidated revenues) in the 1 st quarter of 2017, down

Press release Paris, May 4, 2017 BOURBON 1 st quarter 2017 financial information Adjusted revenues amounted to 225.5 million ( 204.9 million in consolidated revenues) in the 1 st quarter of 2017, down

Investor Presentation

Connecting What s Needed with What s Next Investor Presentation September 2017 Forward-Looking Statements Statements we make in this presentation that express a belief, expectation, or intention are forward

Connecting What s Needed with What s Next Investor Presentation September 2017 Forward-Looking Statements Statements we make in this presentation that express a belief, expectation, or intention are forward

Sanford Bernstein Strategic Decisions Conference. May 2014

Sanford Bernstein Strategic Decisions Conference May 2014 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking statements within the meaning of Section 27A

Sanford Bernstein Strategic Decisions Conference May 2014 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking statements within the meaning of Section 27A

Good resistance for the revenues of BOURBON in a market still with significant decline in activity, but with an oil price that is recovering

Press release Paris, May 4, 2016 BOURBON 1 st 2016 Financial information In the 1 st quarter 2016, BOURBON adjusted revenues reached 314.5 million (-5.9% compared with 4 th quarter 2015), illustrating

Press release Paris, May 4, 2016 BOURBON 1 st 2016 Financial information In the 1 st quarter 2016, BOURBON adjusted revenues reached 314.5 million (-5.9% compared with 4 th quarter 2015), illustrating

2Q 2017 Results. 11 Aug 2017 MERMAID MARITIME PUBLIC COMPANY LIMITED

MERMAID MARITIME PUBLIC COMPANY LIMITED 2Q 2017 Results 11 Aug 2017 1 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated

MERMAID MARITIME PUBLIC COMPANY LIMITED 2Q 2017 Results 11 Aug 2017 1 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated

Mid-Atlantic Investor Meetings. February 2013

Mid-Atlantic Investor Meetings February 2013 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities

Mid-Atlantic Investor Meetings February 2013 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities

Goldman Sachs Global Energy Conference. January 2014

Goldman Sachs Global Energy Conference January 2014 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking statements within the meaning of Section 27A of

Goldman Sachs Global Energy Conference January 2014 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking statements within the meaning of Section 27A of

As anticipated, the offshore oil and gas marine services market is hitting a low point in the second half of 2016.

Press release BOURBON Financial information Q3 and 2016 Paris, November 3, 2016 Adjusted revenues for the first amounted to 858.2 million, down 22.2%; 3 rd quarter adjusted revenues were down 9% compared

Press release BOURBON Financial information Q3 and 2016 Paris, November 3, 2016 Adjusted revenues for the first amounted to 858.2 million, down 22.2%; 3 rd quarter adjusted revenues were down 9% compared

Rod Larson President & CEO

Connecting What s Needed with What s Next Rod Larson President & CEO J.P. Morgan Energy Equity Conference June 27, 2017 New York, NY Forward-Looking Statements Statements we make in this presentation that

Connecting What s Needed with What s Next Rod Larson President & CEO J.P. Morgan Energy Equity Conference June 27, 2017 New York, NY Forward-Looking Statements Statements we make in this presentation that

SOLSTAD OFFSHORE ASA

SOLSTAD OFFSHORE ASA SOLSTAD OFFSHORE ASA 1Q 2012 1. Solstad Offshore in brief 2. Highlights YTD 3. Financials 4. Vessels and markets 5. Outlook SOLSTAD OFFSHORE IN BRIEF Founded in 1964. Head-office in

SOLSTAD OFFSHORE ASA SOLSTAD OFFSHORE ASA 1Q 2012 1. Solstad Offshore in brief 2. Highlights YTD 3. Financials 4. Vessels and markets 5. Outlook SOLSTAD OFFSHORE IN BRIEF Founded in 1964. Head-office in

Capital One Securities, Inc.

Capital One Securities, Inc. 10 th Annual Energy Conference December 9, 2015 New Orleans, LA Alan R. Curtis SVP and Chief Financial Officer Oceaneering International, Inc. Safe Harbor Statement Statements

Capital One Securities, Inc. 10 th Annual Energy Conference December 9, 2015 New Orleans, LA Alan R. Curtis SVP and Chief Financial Officer Oceaneering International, Inc. Safe Harbor Statement Statements

Pareto Securities 20 th Annual Oil & Offshore Conference. Dan Rabun, Chairman & CEO. 4 September 2013

Pareto Securities 20 th Annual Oil & Offshore Conference Dan Rabun, Chairman & CEO 4 September 2013 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking

Pareto Securities 20 th Annual Oil & Offshore Conference Dan Rabun, Chairman & CEO 4 September 2013 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking

Pareto s Annual Oil & Offshore Conference

Pareto s Annual Oil & Offshore Conference Daniel W. Rabun Chairman, President & CEO 31 August 2011 1 Forward-Looking Statements Statements contained in this presentation that are not historical facts are

Pareto s Annual Oil & Offshore Conference Daniel W. Rabun Chairman, President & CEO 31 August 2011 1 Forward-Looking Statements Statements contained in this presentation that are not historical facts are

1Q 2016 Results. Mermaid Maritime Plc. May 23, 2016

Mermaid Maritime Plc 1Q 2016 Results May 23, 2016 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to

Mermaid Maritime Plc 1Q 2016 Results May 23, 2016 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to

Adjusted revenues for the 3 rd quarter recorded a slight rise of 2.6% compared to the previous quarter (consolidated revenues up 4.

Press release BOURBON Financial information 3 rd quarter and 2018 Marseilles, November 8, 2018 Adjusted revenues for the 3 rd quarter recorded a slight rise of 2.6% compared to the previous quarter (consolidated

Press release BOURBON Financial information 3 rd quarter and 2018 Marseilles, November 8, 2018 Adjusted revenues for the 3 rd quarter recorded a slight rise of 2.6% compared to the previous quarter (consolidated

Marvin J. Migura. Oceaneering International, Inc. Executive Vice President. September 30, 2014 New Orleans, LA. Safe Harbor Statement

September 30, 2014 New Orleans, LA Marvin J. Migura Executive Vice President Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express a belief, expectation,

September 30, 2014 New Orleans, LA Marvin J. Migura Executive Vice President Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express a belief, expectation,

2Q 2016 Results. Mermaid Maritime Plc. August 2016

Mermaid Maritime Plc 2Q 2016 Results August 2016 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to

Mermaid Maritime Plc 2Q 2016 Results August 2016 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to

M. Kevin McEvoy. Oceaneering International, Inc. President & CEO. December 2, 2014 New York, NY. Safe Harbor Statement

December 2, 2014 New York, NY M. Kevin McEvoy President & CEO Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express a belief, expectation, or intention

December 2, 2014 New York, NY M. Kevin McEvoy President & CEO Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express a belief, expectation, or intention

Marvin J. Migura. Oceaneering International, Inc. Executive Vice President. Safe Harbor Statement

July 1, 2015 - Houston, TX Marvin J. Migura Executive Vice President Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express a belief, expectation, or

July 1, 2015 - Houston, TX Marvin J. Migura Executive Vice President Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express a belief, expectation, or

Sanford Bernstein Strategic Decisions Conference. May 2013

Sanford Bernstein Strategic Decisions Conference May 2013 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking statements within the meaning of Section 27A

Sanford Bernstein Strategic Decisions Conference May 2013 1 Forward-Looking Statements Statements made today that are not historical facts are forward-looking statements within the meaning of Section 27A

Marvin J. Migura Sr. Vice President & CFO Oceaneering International, Inc.

2009 Energy, Utilities & Power Conference May 27, 2009 Marvin J. Migura Sr. Vice President & CFO Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express

2009 Energy, Utilities & Power Conference May 27, 2009 Marvin J. Migura Sr. Vice President & CFO Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express

Noble Corporation. Don Jacobsen Senior Vice President Industry & Government Relations Marine/Offshore Industry Conference 29 March 2012

Noble Corporation Don Jacobsen Senior Vice President Industry & Government Relations 20 Marine/Offshore Industry Conference 29 March 202 Forward Looking Statement These presentations contain forward-looking

Noble Corporation Don Jacobsen Senior Vice President Industry & Government Relations 20 Marine/Offshore Industry Conference 29 March 202 Forward Looking Statement These presentations contain forward-looking

Marvin J. Migura. Oceaneering International, Inc. Global Hunter Securities 100 Energy Conference June 24, 2014 Chicago, IL. Safe Harbor Statement

Global Hunter Securities 100 Energy Conference June 24, 2014 Chicago, IL Marvin J. Migura Executive Vice President Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation

Global Hunter Securities 100 Energy Conference June 24, 2014 Chicago, IL Marvin J. Migura Executive Vice President Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation

M. Kevin McEvoy. Oceaneering International, Inc. Chief Executive Officer 2015 GLOBAL ENERGY AND POWER EXECUTIVE CONFERENCE JUNE 2, 2015 NEW YORK, NY

2015 GLOBAL ENERGY AND POWER EXECUTIVE CONFERENCE JUNE 2, 2015 NEW YORK, NY M. Kevin McEvoy Chief Executive Officer Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation

2015 GLOBAL ENERGY AND POWER EXECUTIVE CONFERENCE JUNE 2, 2015 NEW YORK, NY M. Kevin McEvoy Chief Executive Officer Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation

Results Briefing Fourth Financial Quarter, 2012* Analyst & Investor Update 20 th December 2012

Results Briefing Fourth Financial Quarter, 2012* Analyst & Investor Update 20 th December 2012 *Financial Quarter ending 30 September 2012 Disclaimer This Analyst Presentation has been prepared by Mermaid

Results Briefing Fourth Financial Quarter, 2012* Analyst & Investor Update 20 th December 2012 *Financial Quarter ending 30 September 2012 Disclaimer This Analyst Presentation has been prepared by Mermaid

Howard Weil Energy Conference

Howard Weil Energy Conference Dan Rabun Chairman, President and CEO 27 March 2012 1 Forward-Looking Statements Statements contained in this press release that are not historical facts are forward-looking

Howard Weil Energy Conference Dan Rabun Chairman, President and CEO 27 March 2012 1 Forward-Looking Statements Statements contained in this press release that are not historical facts are forward-looking

GC RIEBER SHIPPING ASA. /FOURTH QUARTER 2012 PRESENTATION Fourth quarter 2012 Bergen, 22 February Bergen, 25 February 2013

/FOURTH QUARTER 2012 PRESENTATION Fourth quarter 2012 Bergen, 22 February 2013 Bergen, 25 February 2013 Agenda Highlights Q4 2012 Operational review Financial review Summary Outlook / 2 Highlights Fourth

/FOURTH QUARTER 2012 PRESENTATION Fourth quarter 2012 Bergen, 22 February 2013 Bergen, 25 February 2013 Agenda Highlights Q4 2012 Operational review Financial review Summary Outlook / 2 Highlights Fourth

3Q 2016 Results. Mermaid Maritime Plc. 14 November 2016

Mermaid Maritime Plc 3Q 2016 Results 14 November 2016 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed

Mermaid Maritime Plc 3Q 2016 Results 14 November 2016 Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed

Global provider of diversified services and products in all phases of the offshore oilfield life cycle

Investor Presentation January 2017 Forward-Looking Statements Statements we make in this presentation that express a belief, expectation, or intention are forward looking. Forward-looking statements are

Investor Presentation January 2017 Forward-Looking Statements Statements we make in this presentation that express a belief, expectation, or intention are forward looking. Forward-looking statements are

Q1 Financial Presentation 2018 DOF ASA

Q1 Financial Presentation 2018 DOF ASA Highlights Group 2 Highlights EBITDA Q1 MNOK 520 (excl hedge accounting) Average utilisation Group fleet 72% in Q1 Improved markets and signs of higher activity in

Q1 Financial Presentation 2018 DOF ASA Highlights Group 2 Highlights EBITDA Q1 MNOK 520 (excl hedge accounting) Average utilisation Group fleet 72% in Q1 Improved markets and signs of higher activity in

Alan R. Curtis Chief Financial Officer

Connecting What s Needed with What s Next Alan R. Curtis Chief Financial Officer Jefferies Energy Conference November 28, 2017 Houston, TX Forward-Looking Statements Statements we make in this presentation

Connecting What s Needed with What s Next Alan R. Curtis Chief Financial Officer Jefferies Energy Conference November 28, 2017 Houston, TX Forward-Looking Statements Statements we make in this presentation

Q3 Financial Presentation 2017 DOF ASA

Q3 Financial Presentation 2017 DOF ASA Highlights Group 2 Highlights Operational EBITDA Q3 MNOK 607 (excl hedge accounting) Average utilization fleet 73% in Q3 Low utilization in Subsea IRM Projects in

Q3 Financial Presentation 2017 DOF ASA Highlights Group 2 Highlights Operational EBITDA Q3 MNOK 607 (excl hedge accounting) Average utilization fleet 73% in Q3 Low utilization in Subsea IRM Projects in

Quarterly presentation Q DOF Subsea Group

Quarterly presentation Q1 2016 DOF Subsea Group DOF Subsea Group DOF Subsea Group in brief Fleet One of the largest subsea vessel owners in the world Owns and operates a fleet of 21 vessels, plus 4 newbuilds

Quarterly presentation Q1 2016 DOF Subsea Group DOF Subsea Group DOF Subsea Group in brief Fleet One of the largest subsea vessel owners in the world Owns and operates a fleet of 21 vessels, plus 4 newbuilds

Preferred partner. Aker Solutions. Nordic Energy Summit 2013, 21 March Leif Borge CFO

Aker Solutions Nordic Energy Summit 213, 21 March Leif Borge CFO 212 Aker Solutions Slide 1 This is Aker Solutions Employees: 19 5 Contract staff: 5 5 Revenues: 45 bn EBITDA: 4.7 bn Market Cap: 32. bn

Aker Solutions Nordic Energy Summit 213, 21 March Leif Borge CFO 212 Aker Solutions Slide 1 This is Aker Solutions Employees: 19 5 Contract staff: 5 5 Revenues: 45 bn EBITDA: 4.7 bn Market Cap: 32. bn

DNB s oil and offshore conference. Idar Eikrem, CFO

DNB s oil and offshore conference Idar Eikrem, CFO Well positioned for future market opportunities 1) Leading contractor within proven track record 2) Competitive position strengthened a) Delivering projects

DNB s oil and offshore conference Idar Eikrem, CFO Well positioned for future market opportunities 1) Leading contractor within proven track record 2) Competitive position strengthened a) Delivering projects

Simmons & Company International European Energy Conference 2013

Simmons & Company International European Energy Conference 2013 September 27, 2013 Forward-Looking Statements This presentation contains forward-looking statements within the meaning of Section 27A of

Simmons & Company International European Energy Conference 2013 September 27, 2013 Forward-Looking Statements This presentation contains forward-looking statements within the meaning of Section 27A of

September 12,

September 12, 2013 www.deepwater.com The statements described in this presentation that are not historical facts are forward looking statements within the meaning of Section 27A of the Securities Act of

September 12, 2013 www.deepwater.com The statements described in this presentation that are not historical facts are forward looking statements within the meaning of Section 27A of the Securities Act of

Morgan Stanley Houston Energy Summit

Morgan Stanley Houston Energy Summit February 25, 2014 Forward-Looking Statements This presentation contains forward-looking statements that involve risks, uncertainties and assumptions that could cause

Morgan Stanley Houston Energy Summit February 25, 2014 Forward-Looking Statements This presentation contains forward-looking statements that involve risks, uncertainties and assumptions that could cause

Q Presentation. DOF Subsea Group

Q4 2015 Presentation DOF Subsea Group DOF Subsea Group DOF Subsea Group In brief Fleet One of the largest subsea vessel owners in the world Owns and operates a fleet of 21 vessels, plus 4 newbuilds on

Q4 2015 Presentation DOF Subsea Group DOF Subsea Group DOF Subsea Group In brief Fleet One of the largest subsea vessel owners in the world Owns and operates a fleet of 21 vessels, plus 4 newbuilds on

MERMAID MARINE AUSTRALIA LTD. Macquarie Conference May Jeff Weber. We live our values: People Customers Team

MERMAID MARINE AUSTRALIA LTD Macquarie Conference May 2014 Jeff Weber Disclaimer This document contains general background information about the activities of Mermaid Marine Australia Limited (MMA) current

MERMAID MARINE AUSTRALIA LTD Macquarie Conference May 2014 Jeff Weber Disclaimer This document contains general background information about the activities of Mermaid Marine Australia Limited (MMA) current

HY2015. Disciplined performance management. Redefining the future for people and places 1. Attractive growth fundamentals & opportunities

HY2015 Attractive growth fundamentals & opportunities Disciplined performance management Redefining the future for people and places 1 Overview Resilient underlying performance HY2015 Headline EPS 31.3p

HY2015 Attractive growth fundamentals & opportunities Disciplined performance management Redefining the future for people and places 1 Overview Resilient underlying performance HY2015 Headline EPS 31.3p

Swiber Holdings Limited 1Q FY08 Results Briefing

Swiber Holdings Limited 1Q FY08 Results Briefing 15 May 2008 Page 1 Financial Highlights 1Q 2008 Page 2 Key highlights a record quarter Revenue (US$ m) Net Profit (US$ m) 160 1Q Y-O-Y: 266.9% 1Q Y-O-Y:

Swiber Holdings Limited 1Q FY08 Results Briefing 15 May 2008 Page 1 Financial Highlights 1Q 2008 Page 2 Key highlights a record quarter Revenue (US$ m) Net Profit (US$ m) 160 1Q Y-O-Y: 266.9% 1Q Y-O-Y:

Global Offshore Market Challenges

Global Offshore Market Challenges Group Overview DOF ASA in brief Fleet 69 vessels (wholly and partly owned) (19 PSV, 20 AHTS, 30 Subsea) 61 owned vessels in operation 2 owned less than 50% 6 newbuildings;

Global Offshore Market Challenges Group Overview DOF ASA in brief Fleet 69 vessels (wholly and partly owned) (19 PSV, 20 AHTS, 30 Subsea) 61 owned vessels in operation 2 owned less than 50% 6 newbuildings;

Credit Suisse Energy Summit Transocean Ltd.

Credit Suisse Energy Summit Transocean Ltd. February 7, 2012 1 Legal Disclaimer The statements described in this presentation that are not historical facts are forward-looking statements within the meaning

Credit Suisse Energy Summit Transocean Ltd. February 7, 2012 1 Legal Disclaimer The statements described in this presentation that are not historical facts are forward-looking statements within the meaning

GC Rieber Shipping Overall strategy and financial position / PARETO S OIL & OFFSHORE CONFERENCE Oslo, 2 September, 2010 GC RIEBER SHIPPING ASA

/ PARETO S OIL & OFFSHORE CONFERENCE 21 Oslo, 2 September, 21 / 1 GC Rieber Shipping Overall strategy and financial position / 2 / 1 Septem / GC RIEBER SHIPPING S BUSINESS IDEA Industrial company with

/ PARETO S OIL & OFFSHORE CONFERENCE 21 Oslo, 2 September, 21 / 1 GC Rieber Shipping Overall strategy and financial position / 2 / 1 Septem / GC RIEBER SHIPPING S BUSINESS IDEA Industrial company with

Capital Markets Day 31st of May. DOF Group Brazil

Capital Markets Day 31st of May DOF Group Brazil Index I. DOF in Brazil II. Brazilian Offshore Market III. Challenges in Brazil IV. Present/Future outlook DOF ASA 2 DOF ASA DOF Group Brazil Group structure

Capital Markets Day 31st of May DOF Group Brazil Index I. DOF in Brazil II. Brazilian Offshore Market III. Challenges in Brazil IV. Present/Future outlook DOF ASA 2 DOF ASA DOF Group Brazil Group structure

Annual General Meeting

Annual General Meeting 23 rd May 2016 Knots Ahead of the Rest Macro Background Oil price resumed the downtrend in 3 rd Quarter 2015 and bottomed out at USD27 in 1 st Quarter 2016. In 2015, Global E&P capital

Annual General Meeting 23 rd May 2016 Knots Ahead of the Rest Macro Background Oil price resumed the downtrend in 3 rd Quarter 2015 and bottomed out at USD27 in 1 st Quarter 2016. In 2015, Global E&P capital

Corporate Presentation

Corporate Presentation Investor Conference with Credit Suisse Exploration & Production and Offshore & Marine ai Corporate opoaeday 21 22 January 2014, Singapore Disclaimer This presentation has been prepared

Corporate Presentation Investor Conference with Credit Suisse Exploration & Production and Offshore & Marine ai Corporate opoaeday 21 22 January 2014, Singapore Disclaimer This presentation has been prepared

Transition PPT Template. J.P. Morgan. June 2015 V 3.0. Energy Equity Conference June 27, 2017

Transition PPT Template J.P. Morgan June 2015 V 3.0 Energy Equity Conference 2017 June 27, 2017 Forward-Looking Statements This presentation contains forward-looking statements, including, in particular,

Transition PPT Template J.P. Morgan June 2015 V 3.0 Energy Equity Conference 2017 June 27, 2017 Forward-Looking Statements This presentation contains forward-looking statements, including, in particular,

Swiber Holdings Limited

Swiber Holdings Limited 12 months ended 31 Dec 2006 26 February 2007 A niche service provider to the offshore oil and gas industry Forward Looking Statements Important Note The following presentation contain

Swiber Holdings Limited 12 months ended 31 Dec 2006 26 February 2007 A niche service provider to the offshore oil and gas industry Forward Looking Statements Important Note The following presentation contain

Quarterly Presentation Q DOF Subsea Group

Quarterly Presentation Q4 2016 DOF Subsea Group DOF Subsea Group DOF Subsea Group in Brief DOF ASA (51%) First Reserve Corporation (49%) DOF Subsea Holding (100%) DOF Subsea 2005 Established 20 526 NOK

Quarterly Presentation Q4 2016 DOF Subsea Group DOF Subsea Group DOF Subsea Group in Brief DOF ASA (51%) First Reserve Corporation (49%) DOF Subsea Holding (100%) DOF Subsea 2005 Established 20 526 NOK

CANADA S OCEAN SUPERCLUSTER DRAFT NOVEMBER 1

CANADA S OCEAN SUPERCLUSTER AGENDA 01 What is the Ocean Supercluster? 02 What is the opportunity for business? 03 What is the opportunity for Canada? 04 How will the Ocean Supercluster work? 05 What are

CANADA S OCEAN SUPERCLUSTER AGENDA 01 What is the Ocean Supercluster? 02 What is the opportunity for business? 03 What is the opportunity for Canada? 04 How will the Ocean Supercluster work? 05 What are

Conference Call Q2 2013

Conference Call Düsseldorf, July 30, GEA Group Aktiengesellschaft Disclaimer Forward-looking statements are based on our current assumptions and forecasts. These statements naturally entail risks and uncertainties,

Conference Call Düsseldorf, July 30, GEA Group Aktiengesellschaft Disclaimer Forward-looking statements are based on our current assumptions and forecasts. These statements naturally entail risks and uncertainties,

Thinking outside the North Sea. When is global domination not global domination? February 2011

Thinking outside the North Sea When is global domination not global domination? February 2011 ODS-Petrodata is recognised as the leading provider of market intelligence to the global oil and gas industry

Thinking outside the North Sea When is global domination not global domination? February 2011 ODS-Petrodata is recognised as the leading provider of market intelligence to the global oil and gas industry

Forward-Looking Statement

1 Forward-Looking Statement The statements described in this presentation that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and

1 Forward-Looking Statement The statements described in this presentation that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and

Disclaimer Page 2

Disclaimer This presentation should be read in conjunction with Vard Holdings Limited s results for the period ended 31 December 2015 in the SGXNet announcement. Financial figures are presented according

Disclaimer This presentation should be read in conjunction with Vard Holdings Limited s results for the period ended 31 December 2015 in the SGXNet announcement. Financial figures are presented according

Q4 Financial Presentation 2017 DOF ASA

Q4 Financial Presentation 2017 DOF ASA Highlights Group 2 Highlights EBITDA Q4 MNOK 649 (excl hedge accounting) Refinancing completed in DOF and DOF Subsea: Private Placement and repair issue NOK 700 million

Q4 Financial Presentation 2017 DOF ASA Highlights Group 2 Highlights EBITDA Q4 MNOK 649 (excl hedge accounting) Refinancing completed in DOF and DOF Subsea: Private Placement and repair issue NOK 700 million

Boa Offshore update - 3 September Q 14 Results Review Helge Kvalvik, CEO

Boa Offshore update - 3 September 2014 2Q 14 Results Review Helge Kvalvik, CEO Disclaimer This presentation is made by Boa Offshore (or the Company ). The information contained herein include statements

Boa Offshore update - 3 September 2014 2Q 14 Results Review Helge Kvalvik, CEO Disclaimer This presentation is made by Boa Offshore (or the Company ). The information contained herein include statements

Analyst Day Real change starts here. Doug Pferdehirt, Chief Executive Officer

2017 Real change starts here Doug Pferdehirt, Chief Executive Officer Disclaimer Forward-looking statements We would like to caution you with respect to any forward-looking statements made in this commentary

2017 Real change starts here Doug Pferdehirt, Chief Executive Officer Disclaimer Forward-looking statements We would like to caution you with respect to any forward-looking statements made in this commentary

DNB's 9th Annual Oil, Offshore & Shipping Conference Kristian Siem Chairman Subsea 7

DNB's 9th Annual Oil, Offshore & Shipping Conference Kristian Siem Chairman Subsea 7 1 Forward-looking statements Certain statements made in this announcement may include forward-looking statements. These

DNB's 9th Annual Oil, Offshore & Shipping Conference Kristian Siem Chairman Subsea 7 1 Forward-looking statements Certain statements made in this announcement may include forward-looking statements. These

Offshore Support Vessels Located in the US Gulf of Mexico in March 2018

Offshore Support Vessels Located in the US Gulf of Mexico in March 18 IMCA March 1, 18 Prepared by IMCA The International Marine Contractors Association (IMCA) is the international trade association representing

Offshore Support Vessels Located in the US Gulf of Mexico in March 18 IMCA March 1, 18 Prepared by IMCA The International Marine Contractors Association (IMCA) is the international trade association representing

Mermaid Maritime Plc. Corporate Presentation. Investors Non Deal Roadshow February 2014, London. Ready for Growth. maritime.

Corporate Presentation Investors Non Deal Roadshow Maybank a Kim Eng Securities euiie Pte.Ltd. 20 21 February 2014, London Ready for Growth Disclaimer This presentation has been prepared by for shareholders,

Corporate Presentation Investors Non Deal Roadshow Maybank a Kim Eng Securities euiie Pte.Ltd. 20 21 February 2014, London Ready for Growth Disclaimer This presentation has been prepared by for shareholders,

Q Presentation. DOF Subsea Group

Q3 2013 Presentation DOF Subsea Group Agenda In brief Recent events Group overview Contract status Financials Outlook Appendix DOF Subsea DOF Subsea Group In brief Fleet One of the largest subsea vessel

Q3 2013 Presentation DOF Subsea Group Agenda In brief Recent events Group overview Contract status Financials Outlook Appendix DOF Subsea DOF Subsea Group In brief Fleet One of the largest subsea vessel

Quarterly Presentation Q DOF Subsea Group

Quarterly Presentation Q1 2018 Group Group at a glance 2005 established NOK 1.1bn 1) Revenues Q1 18 NOK 15.3bn Firm backlog Q1 18 1 108 2) Subsea employees worldwide Q1 18 Integrated Supplier of subsea

Quarterly Presentation Q1 2018 Group Group at a glance 2005 established NOK 1.1bn 1) Revenues Q1 18 NOK 15.3bn Firm backlog Q1 18 1 108 2) Subsea employees worldwide Q1 18 Integrated Supplier of subsea

A niche service provider to the offshore oil and gas industry. Swiber Holdings Limited Corporate Presentation

A niche service provider to the offshore oil and gas industry Swiber Holdings Limited Corporate Presentation by Raymond Goh, CEO 21 April 2007 A niche service provider to the offshore oil and gas industry

A niche service provider to the offshore oil and gas industry Swiber Holdings Limited Corporate Presentation by Raymond Goh, CEO 21 April 2007 A niche service provider to the offshore oil and gas industry

Corporate Presentation

Corporate Presentation INVEST ASEAN Conference 2014 Maybank Kim Eng Securities Pte. Ltd. 1 2 April 2014, Singapore We help to keep the lights on Disclaimer This presentation has been prepared by for shareholders,

Corporate Presentation INVEST ASEAN Conference 2014 Maybank Kim Eng Securities Pte. Ltd. 1 2 April 2014, Singapore We help to keep the lights on Disclaimer This presentation has been prepared by for shareholders,

T. Jay Collins. President & CEO Oceaneering International, Inc Energy Conference December 7, 2010 New Orleans, LA. Safe Harbor Statement

2010 Energy Conference December 7, 2010 New Orleans, LA T. Jay Collins President & CEO Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express a belief,

2010 Energy Conference December 7, 2010 New Orleans, LA T. Jay Collins President & CEO Oceaneering International, Inc. Safe Harbor Statement Statements we make in this presentation that express a belief,

Spectrum. The Pareto Oil & Offshore Conference. Jan Schoolmeesters, COO. 4 th September 2013

Spectrum at The Pareto Oil & Offshore Conference 4 th September 2013 Jan Schoolmeesters, COO CAUTIONARY STATEMENT This presentation contains both statements of historical fact and forward looking information.

Spectrum at The Pareto Oil & Offshore Conference 4 th September 2013 Jan Schoolmeesters, COO CAUTIONARY STATEMENT This presentation contains both statements of historical fact and forward looking information.

Interim Report. 1 January 30 September Sales declined by 6 percent and reached 9,692 MSEK (10,317) Sales were up 2 percent in local currencies

Sales were up 2 percent in local currencies") Interim Report 1 January 30 September 2003 Sales declined by 6 percent and reached 9,692 MSEK (10,317) Sales were up 2 percent in local currencies Operating income declined to 1,693 MSEK (1,797) or by

Interim Report 1 January 30 September 2003 Sales declined by 6 percent and reached 9,692 MSEK (10,317) Sales were up 2 percent in local currencies Operating income declined to 1,693 MSEK (1,797) or by

FMC Technologies Overview Fourth Quarter Director, Investor Relations Matt Seinsheimer

FMC Overview Fourth Quarter 2016 Director, Investor Relations Matt Seinsheimer +1 281.260.3665 matthew.seinsheimer@fmcti.com This presentation contains forward-looking statements intended to qualify for

FMC Overview Fourth Quarter 2016 Director, Investor Relations Matt Seinsheimer +1 281.260.3665 matthew.seinsheimer@fmcti.com This presentation contains forward-looking statements intended to qualify for

Interim Report Q3 2007

Interim Report Q3 2007 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President and CEO Alfa Laval Group Key figures

Interim Report Q3 2007 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President and CEO Alfa Laval Group Key figures

Alfa Laval Slide 1

Alfa Laval Slide 1 www.alfalaval.com Interim Report Q4 2005 - Orders received, margins and dividend - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström

Alfa Laval Slide 1 www.alfalaval.com Interim Report Q4 2005 - Orders received, margins and dividend - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström

Alfa Laval Slide 1

Alfa Laval Slide 1 www.alfalaval.com Interim Report Q1 2006 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President

Alfa Laval Slide 1 www.alfalaval.com Interim Report Q1 2006 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President

CONSOLIDATED KEY FIGURES 2015

Marine Capability 8 BESIX GROUP IN 2015 CONSOLIDATED KEY FIGURES 2015 RETURN ON EQUITY 0.7% SOLVENCY RATIO 24.4% NET CASH POSITION 26.4 TOP-LINE GROWTH 8.0% in EUR million IN EUR MILLION 2010 2011 2012

Marine Capability 8 BESIX GROUP IN 2015 CONSOLIDATED KEY FIGURES 2015 RETURN ON EQUITY 0.7% SOLVENCY RATIO 24.4% NET CASH POSITION 26.4 TOP-LINE GROWTH 8.0% in EUR million IN EUR MILLION 2010 2011 2012

Pareto Oil & Offshore Conference 2010

Keppel Offshore & Marine Pareto Oil & Offshore Conference 2010 1 2 September 2010 Tong Chong Heong Chief Executive Officer About Keppel Group Keppel Corporation Offshore & Marine Rig building, offshore

Keppel Offshore & Marine Pareto Oil & Offshore Conference 2010 1 2 September 2010 Tong Chong Heong Chief Executive Officer About Keppel Group Keppel Corporation Offshore & Marine Rig building, offshore

Microequities 10th Microcap Conference

Microequities 10th Microcap Conference MATRIX COMPOSITES & ENGINEERING Aaron Begley Chief Executive Officer 5 July 2016 Agenda Company overview Business operations Strategy & outlook 2 What we do Matrix

Microequities 10th Microcap Conference MATRIX COMPOSITES & ENGINEERING Aaron Begley Chief Executive Officer 5 July 2016 Agenda Company overview Business operations Strategy & outlook 2 What we do Matrix

HELIX ENERGY SOLUTIONS

HELIX ENERGY SOLUTIONS OFFSHORE CAPABILITIES www.helixesg.com About Us WELL OPERATIONS SUBSEA WELL INTERVENTION PRODUCTION FACILITIES The purpose-built vessels of our Well Operations business units serve

HELIX ENERGY SOLUTIONS OFFSHORE CAPABILITIES www.helixesg.com About Us WELL OPERATIONS SUBSEA WELL INTERVENTION PRODUCTION FACILITIES The purpose-built vessels of our Well Operations business units serve

QUARTERLY UPDATE. Summary

QUARTERLY UPDATE Q1 FY14 Summary Production levels consistent with designed plant capacity Current order backlog of US$86 million which will support full production until the beginning of Q4 FY14 Strong

QUARTERLY UPDATE Q1 FY14 Summary Production levels consistent with designed plant capacity Current order backlog of US$86 million which will support full production until the beginning of Q4 FY14 Strong

MarketsandMarkets. Publisher Sample

MarketsandMarkets http://www.marketresearch.com/marketsandmarkets-v3719/ Publisher Sample Phone: 800.298.5699 (US) or +1.240.747.3093 or +1.240.747.3093 (Int'l) Hours: Monday - Thursday: 5:30am - 6:30pm

MarketsandMarkets http://www.marketresearch.com/marketsandmarkets-v3719/ Publisher Sample Phone: 800.298.5699 (US) or +1.240.747.3093 or +1.240.747.3093 (Int'l) Hours: Monday - Thursday: 5:30am - 6:30pm

Textron Reports Third Quarter 2014 Income from Continuing Operations of $0.57 per Share, up 62.9%; Revenues up 18.1%

Textron Reports Third Quarter Income from Continuing Operations of $0.57 per Share, up 62.9%; Revenues up 18.1% 10/17/ PROVIDENCE, R.I.--(BUSINESS WIRE)-- Textron Inc. (NYSE: TXT) today reported third

Textron Reports Third Quarter Income from Continuing Operations of $0.57 per Share, up 62.9%; Revenues up 18.1% 10/17/ PROVIDENCE, R.I.--(BUSINESS WIRE)-- Textron Inc. (NYSE: TXT) today reported third

Quarterly Presentation Q DOF Subsea Group

Quarterly Presentation Q3 2017 Group highlights 1 Attractive long-term market fundamentals supporting continued demand for subsea offshore solutions 2 A true global subsea IMR operator with strong project

Quarterly Presentation Q3 2017 Group highlights 1 Attractive long-term market fundamentals supporting continued demand for subsea offshore solutions 2 A true global subsea IMR operator with strong project

Hunting PLC Annual Results 2010

Hunting PLC Annual Results 2010 2010 Highlights Completed acquisition of Innova-Extel - 80.3m New facilities in US (Casper, Conroe and Latrobe) and China (Wuxi) add over 800,000 sq ft of manufacturing

Hunting PLC Annual Results 2010 2010 Highlights Completed acquisition of Innova-Extel - 80.3m New facilities in US (Casper, Conroe and Latrobe) and China (Wuxi) add over 800,000 sq ft of manufacturing

MPF Corp. Ltd. Pareto Conference September 6 th, 2006

MPF Corp. Ltd. Pareto Conference September 6 th, 2006 The Multi Purpose Floater (MPF) Drilling, production, storage and offloading capabilities in one unit 6th generation drilling facility 1 million barrels

MPF Corp. Ltd. Pareto Conference September 6 th, 2006 The Multi Purpose Floater (MPF) Drilling, production, storage and offloading capabilities in one unit 6th generation drilling facility 1 million barrels

Quarterly Presentation Q DOF Subsea Group

Quarterly Presentation Q4 2017 Group Group at a glance 2005 established NOK 4.6bn 1) Revenues 2017 NOK 16.1bn Firm backlog Q4 17 1 214 2) Subsea employees worldwide Q4 17 Integrated Supplier of subsea

Quarterly Presentation Q4 2017 Group Group at a glance 2005 established NOK 4.6bn 1) Revenues 2017 NOK 16.1bn Firm backlog Q4 17 1 214 2) Subsea employees worldwide Q4 17 Integrated Supplier of subsea

Textron Reports Second Quarter 2014 Income from Continuing Operations of $0.51 per Share, up 27.5%; Revenues up 23.5%

Textron Reports Second Quarter 2014 Income from Continuing Operations of $0.51 per Share, up 27.5%; Revenues up 23.5% 07/16/2014 PROVIDENCE, R.I.--(BUSINESS WIRE)-- Textron Inc. (NYSE: TXT) today reported

Textron Reports Second Quarter 2014 Income from Continuing Operations of $0.51 per Share, up 27.5%; Revenues up 23.5% 07/16/2014 PROVIDENCE, R.I.--(BUSINESS WIRE)-- Textron Inc. (NYSE: TXT) today reported

DIGITALISATION OFFSHORE

aveva.com DIGITALISATION OFFSHORE Is it the secret to sustaining lower operating costs? EXECUTIVE SUMMARY September 2017 EXECUTIVE SUMMARY 2 The offshore oil and gas production sector has been particularly

aveva.com DIGITALISATION OFFSHORE Is it the secret to sustaining lower operating costs? EXECUTIVE SUMMARY September 2017 EXECUTIVE SUMMARY 2 The offshore oil and gas production sector has been particularly

Matrix Composites & Engineering Ltd

Matrix Composites & Engineering Ltd Euroz 2015 Industrials Tour 10 June 2015 Overview Introduction to Matrix Business Operations and Outlook Plant Tour 2 Introduction to Matrix WHO WE ARE AND WHAT WE DO

Matrix Composites & Engineering Ltd Euroz 2015 Industrials Tour 10 June 2015 Overview Introduction to Matrix Business Operations and Outlook Plant Tour 2 Introduction to Matrix WHO WE ARE AND WHAT WE DO

Internationalization of the Norwegian Supply and Service Industry with focus on Brazil

Internationalization of the Norwegian Supply and Service Industry with focus on Brazil The role of Pre Sal S/A Approach to Norwegian Institutions and Industry 12 August 2015 Country Manager - Brazil Adhemar

Internationalization of the Norwegian Supply and Service Industry with focus on Brazil The role of Pre Sal S/A Approach to Norwegian Institutions and Industry 12 August 2015 Country Manager - Brazil Adhemar

Emergency Pipeline Repair Systems; A Global Overview of Best Practice

Emergency Pipeline Repair Systems; A Global Overview of Best Practice Brief Introduction to EPRS EPRS: Key Challenges Worldwide EPRS: Global Approaches to These Challenges Best Practice Comparison James

Emergency Pipeline Repair Systems; A Global Overview of Best Practice Brief Introduction to EPRS EPRS: Key Challenges Worldwide EPRS: Global Approaches to These Challenges Best Practice Comparison James

Alfa Laval Slide 1

Alfa Laval Slide 1 www.alfalaval.com Interim Report Q2 2008 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President

Alfa Laval Slide 1 www.alfalaval.com Interim Report Q2 2008 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President

Erratum to the Press Release 2017 annual results - NRJ Group. dated March 15, 2018

Paris, March 20, 2018 5:45 pm Erratum to the Press Release 2017 annual results - NRJ Group dated March 15, 2018 An editorial error was made in the press release dated March 15, 2018 (English version only)

Paris, March 20, 2018 5:45 pm Erratum to the Press Release 2017 annual results - NRJ Group dated March 15, 2018 An editorial error was made in the press release dated March 15, 2018 (English version only)

Pareto Oil & Offshore Conference 6 September 2006 CEO Terje Sørensen

Pareto Oil & Offshore Conference 6 September 2006 CEO Terje Sørensen Strategy To grow the company within offshore support vessels Seek to combine with other operators in the same field, in order to achieve

Pareto Oil & Offshore Conference 6 September 2006 CEO Terje Sørensen Strategy To grow the company within offshore support vessels Seek to combine with other operators in the same field, in order to achieve

2011 Capital Markets Day

2011 Capital Markets Day Geir Håøy President Kongsberg Maritime WORLD CLASS through people, technology and dedication Kongsberg Maritime Introduction Significant market position within the drilling segment

2011 Capital Markets Day Geir Håøy President Kongsberg Maritime WORLD CLASS through people, technology and dedication Kongsberg Maritime Introduction Significant market position within the drilling segment

Wood Group Investor Briefing Q1 2016

Wood Group Investor Briefing Q1 2016 Our business Wood Group is an international projects, production and specialist technical solutions provider with around $6bn sales and 36,000 employees. We are focused

Wood Group Investor Briefing Q1 2016 Our business Wood Group is an international projects, production and specialist technical solutions provider with around $6bn sales and 36,000 employees. We are focused

Capital Marked Presentation. Dof Subsea Atlantic Region

Capital Marked Presentation Dof Subsea Atlantic Region Agenda Atlantic Business and Area of Operation Clients & Some Ongoing Contracts Our Capabilities Market Outlook DOF Subsea 2 Atlantic Business and

Capital Marked Presentation Dof Subsea Atlantic Region Agenda Atlantic Business and Area of Operation Clients & Some Ongoing Contracts Our Capabilities Market Outlook DOF Subsea 2 Atlantic Business and

Confirms 2013 Financial Guidance

Confirms 2013 Financial Guidance PROVIDENCE, R.I.--(BUSINESS WIRE)--Jul. 17, 2013-- Textron Inc. (NYSE: TXT) today reported second quarter 2013 income from continuing operations of $0.40 per share, compared

Confirms 2013 Financial Guidance PROVIDENCE, R.I.--(BUSINESS WIRE)--Jul. 17, 2013-- Textron Inc. (NYSE: TXT) today reported second quarter 2013 income from continuing operations of $0.40 per share, compared

Q Presentation Preliminary Results FY 2011

Presentation Preliminary Results FY Düsseldorf, February 6, 2012 GEA Group Disclaimer All figures for are preliminary and have therefore not yet been audited. The yearend financial statements for the GEA

Presentation Preliminary Results FY Düsseldorf, February 6, 2012 GEA Group Disclaimer All figures for are preliminary and have therefore not yet been audited. The yearend financial statements for the GEA

Alfa Laval Slide 1

Alfa Laval Slide 1 www.alfalaval.com Interim Report Q1 2008 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President

Alfa Laval Slide 1 www.alfalaval.com Interim Report Q1 2008 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President

Alf a Lav al Slide 1

Alf a Lav al Slide 1 www.alfalaval.com Interim Report Q2 2007 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President

Alf a Lav al Slide 1 www.alfalaval.com Interim Report Q2 2007 - Orders received and margins - Highlights - Development per segment - Geographical development - Financials - Outlook Mr. Lars Renström President